LONDON/HOUSTON/SINGAPORE, June 18: The next generation of AI agents could consume between 10,000 and 40,000 times more computing power per task than today’s chatbots. That pressure is pushing some of the world’s largest technology companies to consider putting their data centres in space. A new report from Wood Mackenzie finds they face a significant cost problem to get there.

Global data centre power demand stands at 460 TWh in 2026, equivalent to half of Japan’s total power generation. Wood Mackenzie forecasts that figure will reach 1,280 TWh by 2030 and 3,700 TWh by 2040, a 703% increase from current levels, growing at 16% per year. The United States and China together account for 78% of the global planned data centre pipeline.

On the ground, that pipeline is running into real constraints. Grid connections in the United States can take up to seven years. Gas turbine equipment faces long wait times through 2030. In dry regions, cooling systems are competing for limited water supplies. Construction costs are rising from higher labour and material costs. These bottlenecks, Wood Mackenzie concludes, are driving serious exploration of orbital data centres.

The economics are not yet close.

A hypothetical 1 GW orbital data centre would cost an estimated US$170 billion, more than three times the equivalent terrestrial facility, with launch and satellite costs accounting for approximately 60% of that total. To bring orbital costs to parity with terrestrial alternatives would require a 70% reduction. That is achievable, the report notes, only if the historical trend of exponential cost declines in space launch continues.

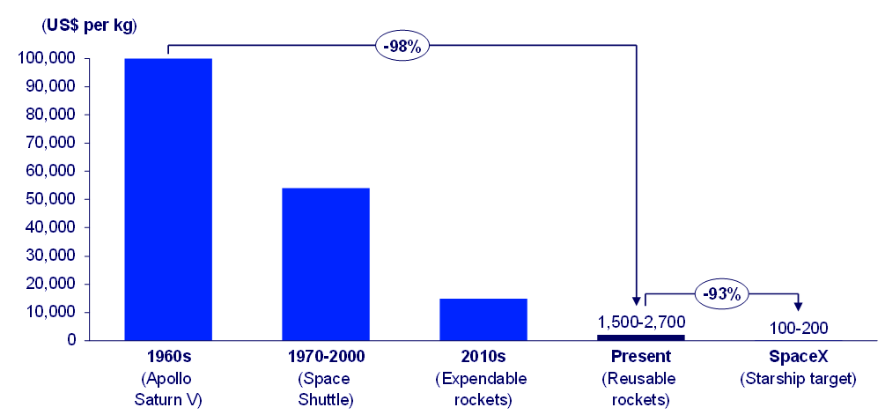

There is reason to think it might. Global orbital launch attempts reached 324 in 2025, a 25% increase over 2024, with commercial operators conducting 70% of those attempts. Launch costs have already fallen approximately 90% with current-generation reusable rockets compared to their expendable predecessors. A record 4,517 satellites were deployed into orbit in 2025, 58% more than the previous year, with 87% owned by private entities.

SpaceX and xAI have announced ambitious plans to put 100 GW of orbital computing capacity into space annually, a figure ten times the combined announced pipeline of every other orbital data centre developer in the world. Non-US companies account for less than 0.5 GW of total planned orbital capacity, reflecting how concentrated this emerging sector is among US-based firms. Despite the higher costs, launch activities across the top five companies are expected to begin accelerating between 2027 and 2028.

Space launch costs have seen exponential cost declines of over 90%

Source: Wood Mackenzie

Spending on terrestrial capacity has not slowed in the meantime. Anthropic recently committed US$ 45 billion over three years to SpaceX for access to its 300 MW Colossus 1 terrestrial data centre, deploying 220,000 Nvidia GPUs. Wood Mackenzie forecasts US$ 9 trillion in cumulative capital expenditure between 2026 and 2040 to build approximately 395 GW of new terrestrial data centre capacity under its base case.

“The constraints on terrestrial data centres are genuine, and they are not going away quickly,” said Robert Liew, Research Director at Wood Mackenzie. “But putting a data centre in orbit still costs at least three times as much as building one on the ground. That gap does not close without sustained and dramatic progress on launch costs. We forecast US$ 9 trillion of terrestrial data centre investment between now and 2040. That is where capital goes first. Orbital data centres are a serious long-term proposition, but right now they remain a bet on the cost curve.”

Wood Mackenzie’s base case energy transition outlook does not include large-scale orbital data centres. No gigawatt-scale orbital or terrestrial facility currently exists. The report concludes that terrestrial build-out will be driven by necessity, while orbital data centres remain, for now, a technology preference.